Italy's fake economic boom - Draghinomics #3

Italy's fake economic boom - Draghinomics #3

GDP grows but perspective matters

"GDP surge", "growth at its highest", "never so high since 1976". Reading the newspapers, it seems that Italy is experiencing a new economic boom. However, looking at the complete data - and especially putting it into perspective - the situation that emerges is not so rosy.

Let's start with economic growth. According to the preliminary estimate released by ISTAT on 31 January, in 2021 GDP increased by 6.5% compared to 2020. The big press, which sees la vie en rose, and several ministers did not hold back their "great satisfaction".

Such a high growth rate has not been seen since the 1970s. A leitmotif launched during the ISTAT press conference by Giovanni Savio (central director of national accounts) and immediately ended up in the headlines of Il Sole 24 Ore, Corriere della Sera, La Stampa and La Repubblica.

But focusing only on growth rates gives a distorted perspective. To get a more balanced viewpoint, one need only consider that a recession like the one in 2020 has not been seen since the Second World War, as Savio himself pointed out. This is the other side of the coin, which many commentators do not consider so much.

GDP growth of 6.5% in 2021 is more of a rebound than a real "leap". In fact, in 2020 the Italian economy contracted by 9% and it is natural that then (with the easing of restrictive measures, the full activation of automatic stabilisers and the necessary counter-cyclical public spending) we returned to greater activity. In other words, with the crisis we fell down a steep mountain, and now we are simply climbing back up.

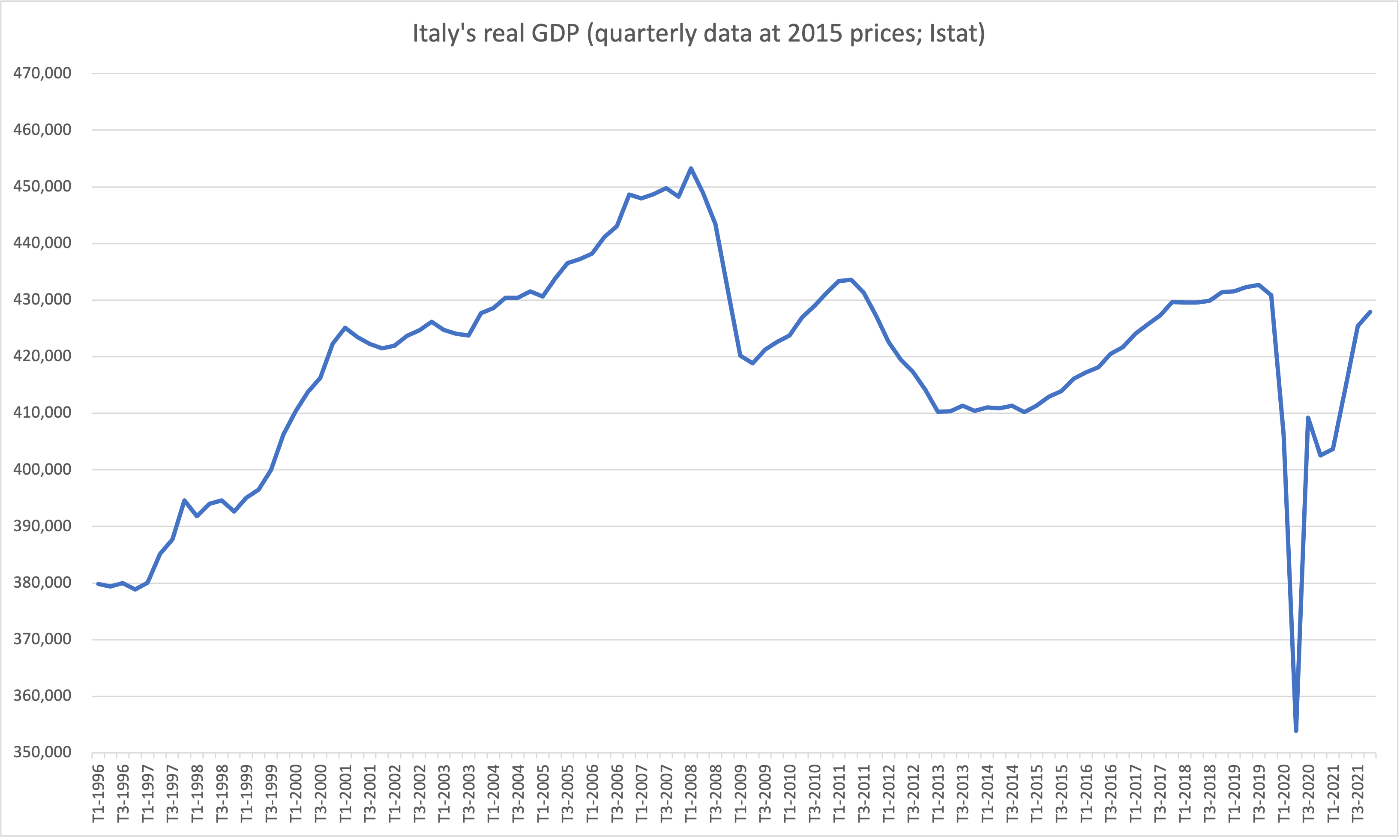

To put things in perspective, a simple exercise is all that is needed. Let's take the quarterly ISTAT data and supplement them with one of the other estimates just released: +0.6% real growth between Q3 and Q4 2021. What we get is the following graph, where we see that we have not yet recovered the pre-Covid GDP of 2019.

For its part, the government has set itself the target of "achieving GDP growth of more than 4% in 2022", according to a note from the Ministry of Economy (in the budget the forecast is 4.7%). If the OECD in its latest Outlook has even estimated a growth of 4.6% for 2022, the Bank of Italy and the International Monetary Fund are not of the same opinion, with both estimates stopping at 3.8%.

With this further growth, GDP would finally recover its pre-pandemic level, but would still remain below the eurozone average. Clearly, in such a situation, it is not enough simply to go back to where Covid took us by surprise. It is worth remembering that before the pandemic Italy had not yet recovered to the levels of economic activity that existed before the 2008 crisis. The Next Generation EU money continues to be invoked as a panacea, but it will not be enough to heal the weaknesses of the Italian economy.

On the employment side, too, the figures show that what appears to be growth is in fact only a very partial recovery from the slump experienced in 2020. Among other things, with a far more marked dose of precariousness than that seen before the pandemic.

One number above all: in December 2021, the total number of people employed in Italy was still 286,000 lower than in February 2020, the month in which the virus broke out.

But it is above all if we look at the quality of new hires that the weakness of this recovery comes to light. Also in the last month of 2021, fixed-term employees reached 3.77 million. We are a step away from the historical record of three million and 97 thousand obtained in May 2018, before the arrival of the so called Dignity Decree (under the League-Five Star coalition government).

In the last quarter of last year, the only employment contracts that show a positive balance - plus 92 thousand - are the precarious ones, while the permanent ones are down by 17 thousand. But it is a dynamic that concerns the whole of 2021: on an annual basis, between December 2020 and December 2021, subordinate jobs rose by 590 thousand units, and of these as many as 434 thousand - 73.6% - are fixed-term.

In recent times, Confindustria (Confederation of Italian Industry) has often called for the government's help, claiming, in words, to want to create good jobs; this desire seems so far to have been held back by a lack of confidence on the part of the companies themselves in the growth prospects or by the desire to cut costs. At least for the time being, they are recruiting three quarters of new employees with fixed-term contracts and more than a third part-time.

This type of employment mainly concerns women. According to the Gender Policies Report published a few weeks ago by Inapp, in the first half of 2021 more than 3.3 million employment relationships were activated, and of these almost 1.2 million were part-time. The incidence is as high as 65% in the public administration, education and health sector, 55% in real estate and 42.6% in trade and tourism. As many as 49.6% of women employed had to make do with contracts of just a few hours.

This is a general figure for Italy in which, as always, there is a very varied situation between different regions and between cities and suburbs. In Calabria, for example, 74.4% of women's contracts are part-time. The percentage in the other Southern regions is slightly lower.

This large number of contracts means that the total number of hours worked remains constantly below pre-pandemic levels. In the third quarter of 2021 they stopped just below 10.5 billion. In the same quarter of 2019, they exceeded 11 billion. Precarious and fragile employment relationships produce poor wages.

The mix of low wages and low number of hours worked squeezes workers' earnings. In 2021, contractual hourly wages rose by 0.6%, much less than inflation growth. As ISTAT explained, "in the light of the consumer price dynamic - which accelerated sharply in the second half of the year and is about three times the wage dynamic - there is also a reduction in purchasing power".

This article was written by Alessandro Bonetti and Roberto Rotunno and published on the 2nd of February on Il Fatto Quotidiano.